News & Insights Assessing the impact your business model & technology partner has on profit

Financial planning principals are continuously faced with the pressure of legislative change, and there is very little air time between articles referencing the Royal Commission, FASEA and other regulatory changes. These factors all have the ability to significantly impact profit, which can trigger advice firms to analyse and re-evaluate what’s important to their planning practice, their client base and ultimately their future business success.

This paper examines some of the factors that can impact a planning practice’s business model, including general barriers to innovation and collaboration, and will outline why platform choice will be more of a strategic business decision in the future rather than just an investment transaction. This paper will also review the impact that the choice of business model can have on profit, utilising independent research on practices embracing managed accounts, and will provide considerations for selecting the most suitable technology and insights for those looking to innovate and transform their business.

The innovation and collaboration conundrum

In an environment of high-profile legislation requiring stringent compliance oversight, business owners and practice managers can view regulation as a significant barrier to success. However, the contingent continuing to grow their businesses are faced with the same legislative pressures, access to resources and available investor communities. Whilst it is impossible not to sympathise with those feeling the pressure, the main difference between growth and stagnation is often the mindset of the principal or business manager.

The small-to-medium enterprise (SME) sector covers microbusinesses (1–4 employees), small businesses (5–19) and medium businesses (20–199), and makes up 98% of all Australian businesses, producing one-third of the total GDP. The majority of the financial planning fraternity sits firmly within the micro and small business component of this sector, with some larger practices entering into the medium business category. There would therefore be many correlations between financial planning practices in Australia and the wider business community, and one concerning theme is the challenge of innovation and/or collaboration.

According to the Global Innovation Index (www.globalinnovationindex.org), Australia ranks 22nd in the 2019 list, behind much smaller economies. We need to seriously consider why that is the case. In the instance of the SME sector and relevant financial services business owners, it could be suggested that, when a business owner or individual considers innovation, it is at a transformational level. Due to the enormity of activity that a business transformation requires, it often stymies any action at all. The requirement to focus on day-to-day activity just adds to this pressure, and business owners find themselves putting off change to a later date.

Many technology reviews take place after the ‘successful’ visit of a platform or technology representative who has managed to disturb the status quo and alert the interest of a decision-maker. Thereafter, any further review is based on what a piece of technology can do rather than what a business owner needs it to do. Furthermore, without foresight, how can you review something without a clear set of parameters and controls with which to benchmark it? Ricoh, a workplace technology specialist, has researched and commented that 60% of Australian organisations do not have a detailed enough level of clarity around required systems and processes, and this is holding back increases in production efficiency.

According to the ABS (Innovation of Business, 2016-17), Australia’s slow move towards innovation is clearly demonstrated by the fact that:

- only 31% of microbusinesses and 50% of small businesses have actually introduced innovation and;

- only 13% of microbusinesses and 22% of small businesses introduced new or significantly improved operational processes during 2016-17.

With no clear parameters around business needs or a defined client engagement model, it is not surprising that this is the result. What often occurs when practices move to a Managed Account solution is that they do so with a small set of internalised tactical objectives, such as removal of RoA obligations to relieve the compliance burden, rather than with an overall enduring strategic vision for the practice and its clients.

The Managed Account industry has dramatically changed the technology landscape in recent times. Excitingly, innovations in API access, machine learning and new technology are driving daily change to solutions and services offered by incumbents and new entrants. This is driving the need for practice owners and managers to partner with providers that can offer insight into best practice principles, help navigate the strategic landscape and assist in managing new legislative hurdles.

However, despite this opportunity there are some startling statistics that show:

- Only 18% of innovative business owners collaborate with others around innovation.

- Only 5.5% of overall microbusinesses collaborate outside their business; and

- Only 9% of small business owners collaborate outside their business.

This is a surprising outcome and demonstrates that business owners face a real challenge to not only embrace change, but to source IP from alternate sources.

When you consider the isolation of many micro or small business owners, and their often lack of or limited access to resources with which to invest in infrastructure and people, it would make intuitive sense to source IP from external sources. Yet businesses that are rated as innovative by the ABS stated that there are factors preventing or limiting collaboration – 10% stated that it was partly due to them seeing no value in collaboration and 20% said it was partly due to a lack of time and funds. Unsurprisingly, 56% stated that there were no factors affecting collaboration other than personal choice!

So, what does this mean for the financial services sector and the SMEs within it?

There are three main considerations

- Inertia will continue to restrict profit growth, increase business valuation risk and limit the ability of business owners to keep pace with changing client demands.

- Business owners and practice managers need to have a very clear sense of strategic direction and short-term tactical priorities in order to ensure that processes and services remain relevant.

- Collaboration is being ignored by many, and business owners are going it alone. There is an opportunity to engage with suppliers, clients and peers to more successfully navigate the short to medium term.

Choosing a technology partner that is not only right for a business today but in the future has never been more important. Tapping into the innovation insights, technology and market expertise the right technology partner can offer can support true business transformation.

Australia’s platform industry competes furiously to be a firm’s partner of choice with many adopting pricing strategies as a means of attracting and retaining clients. If choice was based solely on price then we would have a far simpler industry, but it is not that simple. Of course, cost needs to be a competitive pressure, however value in terms of platform choice goes well beyond just price.

Planning firms need to have a clear understanding of not only their current needs but also their future requirements and select a platform partner that can support them in achieving their objectives, which is why platform choice in the future needs to become a strategic decision for practices.

Why choosing a platform in future will be more of a strategic business decision?

Adviser business models have remained fairly consistent in the last decade. This doesn’t mean there haven’t been significant changes to business processes, but the change has mainly been forced upon practices by legislation as firms worked through FoFA and the Royal Commission.

However, we continue to see a seismic shift in client needs and the expectations they have of their advisers that could equally impact a firm’s bottom line. With information at their fingertips and the ability to complete their own research before embarking on their investment journey, investors can now access robo-advice solutions, providing low entry levels to those wishing to start investing. With 75% of consumers preferring to self-solve their own customer service issue, providing a digital solution as part of their value proposition is becoming increasingly important for advice firms in servicing this changing client profile.

An exciting opportunity is the well-documented fact that in the next three decades, $3 trillion in assets will move from one generation to the next in Australia. In the US, the transfer is estimated to be well over $30 trillion, and worldwide the figures are staggering. The question is, how well placed are practice owners to take advantage of this wealth shift, given statistics show that 90% of inheritors typically change advisers upon receiving their inheritance? Retaining the next generation of clients is a significant challenge for the advice industry, to ensure profit and business valuations are maintained.

Managed accounts, and importantly the choice of technology platform partner, can help practices on both these fronts. However, not all managed accounts platforms are the same. As such, when business owners and practice managers research the market, they need to be very clear on the differences.

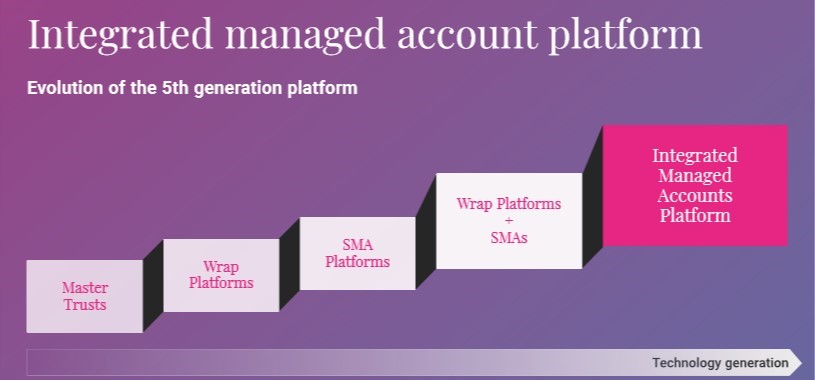

The platform landscape has changed significantly over the past 25 years. In the early 1990s we saw the development of Master Trusts as the first platform structure to consolidate investment execution and reporting and simplify the investment experience for investors and their advisers. Next came wrap platforms, which facilitated broader investment choice (e.g. listed securities), broader overarching reporting across super and ordinary investment savings, lower investor costs, greater advice fee collection functionality and the introduction of adviser- and dealer-level model portfolio functionality. In more recent times, many wrap platforms have, with varying degrees of success, attempted to add on SMAs and associated functionality. This has been a difficult undertaking for some since the technology requirements for running non-unitised, actively managed investment portfolios are fundamentally different to wraps, which are essentially investment administration services.

The way has been paved for groups such as Praemium and others innovating at a fast pace to deliver deeper solutions such as the next-generation integrated managed accounts platform (See diagram below), which caters for all managed accounts structures on a single platform to deliver more efficiency and client engagement than ever before

A next-gen integrated managed accounts platform includes simple and consolidated reporting of all investment assets (including custody and non-custody); broad investment choice with ease and flexibility to make changes; tailored solutions for every kind of investor; administrative accuracy and efficiency; and the benefit of platform scale in the form of very competitive fees at all levels.

This change has happened extremely quickly, as planning practices seek greater efficiency to better respond to legislative change and client demands that are putting pressure on existing business models. The need to understand the complexity of each platform and understand how new systems will assist in increasing profits, drive client engagement and minimise risk is imperative for planning practices. This is especially prevalent as institutionally restricted practices open up their APL opportunities and move to self or independent licensing environments and need to compare and assess next-gen solutions with their wrap counterparts.

Therefore, choosing a platform in future will irrefutably be more of a strategic business decision than a tactical investment solution. Should business owners and practice managers get it right, though, the effect on profits can be significant.

Driving profit through Managed Accounts solutions

Each planning practice has its own unique business needs, appropriate KPIs and ‘ideal’ client profile. Geographical location and business model will drive a different set of influences on client engagement models. However, delivering greater efficiencies, driving greater profit, retaining clients and increasing client acquisition is a consistent requirement across every SME.

Business Health, a leading practice management provider in Australia, utilise their proprietary diagnostic tool, the Business HealthCheck, to assist practice owners to benchmark their business against industry peers and their competitive universe to drive business success. Of those practices that have utilised the HealthCheck, Business Health have been able to analyse the practices that use Managed Accounts and benchmark against those that don’t to determine the impact that using Managed Accounts has on their business.

Their analysis shows that:

- 47% of practices have access to SMAs on their APL; and

- 37% have access to MDA solutions, a significant growth in this sector.

Furthermore:

- 27% of diagnostic participants utilising managed accounts use the solution for all their clients;

- 45% utilise them for larger clients over $200k; and

- 33% use managed accounts as a replacement for traditional direct equity solutions.

With a sizeable percentage utilising managed account technology, it is interesting to understand the impact that embracing managed accounts in some form has on various factors and the uplift this delivers relative to firms that do not use managed accounts at all.

| Factor | Uplift |

| Revenue per FTE adviser | 22.6% |

| Notional practice profit | 21.3% |

| Notional profit per client | 28.8% |

| Clients per advisers | 12.4% |

| Client appointments per adviser per week | -6.5% |

| 20+ clients added in the past 12 months | 7.7% |

The analysis above clearly demonstrates that the rhetoric around the use of managed account technology and its impact on business profit is accurate. As the industry harnesses enhanced best practice models through increased experience in this sector, it is likely that we will see these divergences between users and non-users increase.

Interestingly, previous practice management methodology talked about reducing numbers of clients, through ideal client profiling techniques, to focus on more profitable clients. The analysis above is showing that the number of clients can increase whilst still maintaining profit levels by taking advantage of scalable technology solutions to drive engagement to a wider audience. This was very difficult until recently, and managed accounts coupled with next-gen platforms are definitely making this a real business benefit and strategy.

Finally, the analysis also highlights that those using managed accounts see an increase in client acquisition. This could be as a result of businesses having more time for marketing and prospecting activities due to the efficiencies gained through using this technology. It will be interesting to see, as more practices harness next-gen platforms with their enhanced client-centric value propositions, if client acquisitions continue to increase. Clients refer experiences, not things. The simple connection that a better digital experience offers can be a driver of client referrals and should be a criterion for deciding which technology provider to partner with.

Business owners and practice managers can harness managed accounts and next-gen platforms to truly transform their business, or at the very least solve a number of key business barriers and priorities. To do so they should:

» Embrace an innovative culture

» Understand their business strategy and value proposition

» Ensure they understand the generational version of the platform they are using

» Collaborate and partner as much as possible.

Upgrade today!

Start the upgrade now. Ask our expert team about the ways

Morningstar Wealth Platform can transform your business.